Choice Made Simple!

Too many options?Click below to purchase an online gift card that can be used at participating retailers in Village Green Shopping Centre and continue your shopping IN CENTRE!Purchase HereHome

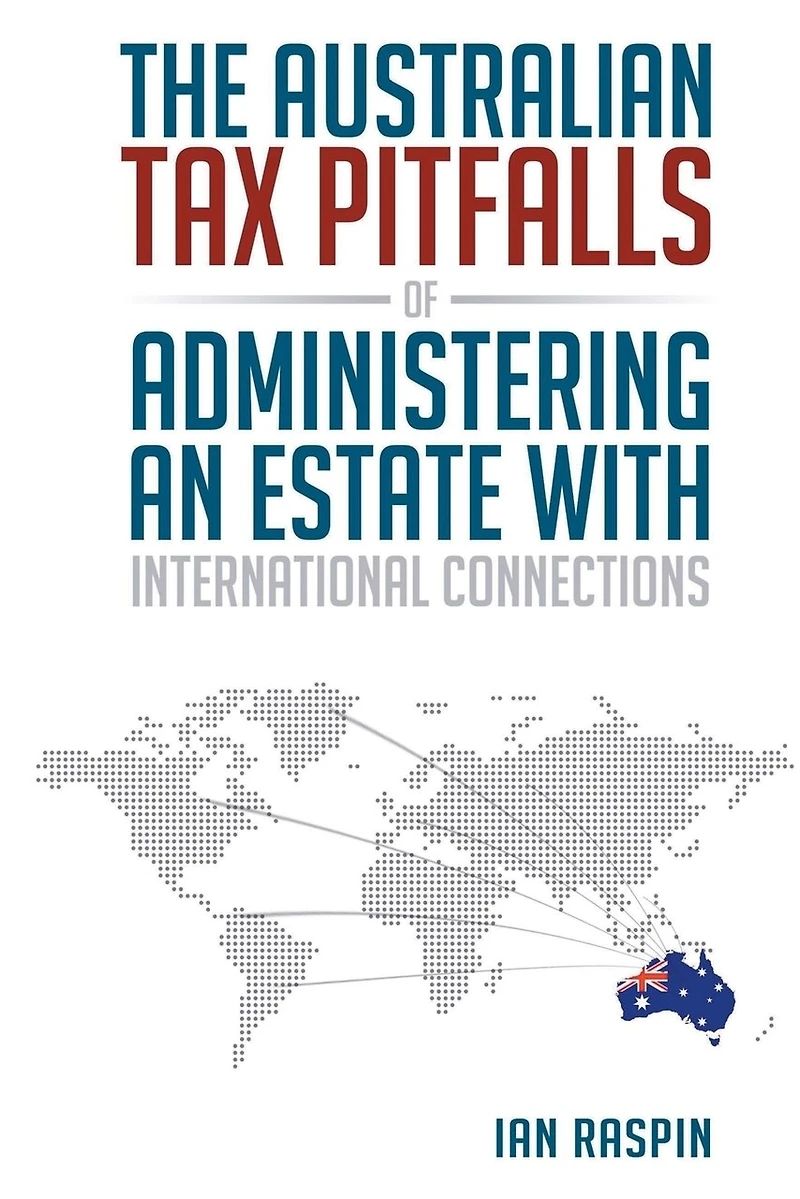

Administering an Estate with International Connections: Australian Tax Pitfalls

Coles

Loading Inventory...

Administering an Estate with International Connections: Australian Tax Pitfalls in Vernon, BC

By None

Current price: $32.50

Coles

Administering an Estate with International Connections: Australian Tax Pitfalls in Vernon, BC

By None

Current price: $32.50

Loading Inventory...

Size: Paperback

*Product information may vary - to confirm product availability, pricing, shipping and return information please contact Coles

It's true, the world is becoming a smaller place. With increased global mobility, estate practitioners are having to grapple more with international aspects of estate administration. This book is intended to provide estate practitioners with an overview of some of the Australian tax issues that they should be aware of when involved with the administration of an estate where: -the deceased was previously a foreign resident -some of the beneficiaries are foreign residents -the deceased owned foreign assets (or non-taxable Australian property assets), or -the executor or legal personal representative is a foreign resident. It is hoped that this book will serve as a valuable reference tool and help legal practitioners and associated parties navigate their way through the inherently complex Australian income tax laws when administering an estate with international connections. Throughout this book the terms 'foreign resident' and 'non-resident' are used interchangeably and have the same definition. This anomaly in terminology occurs as Income Tax Assessment Act 1936 (Cth) ('ITAA 1936') uses the term 'non-resident' while Income Tax Assessment Act 1997 (Cth) ('ITAA 1997') primarily uses the term 'foreign resident'.

It's true, the world is becoming a smaller place. With increased global mobility, estate practitioners are having to grapple more with international aspects of estate administration. This book is intended to provide estate practitioners with an overview of some of the Australian tax issues that they should be aware of when involved with the administration of an estate where: -the deceased was previously a foreign resident -some of the beneficiaries are foreign residents -the deceased owned foreign assets (or non-taxable Australian property assets), or -the executor or legal personal representative is a foreign resident. It is hoped that this book will serve as a valuable reference tool and help legal practitioners and associated parties navigate their way through the inherently complex Australian income tax laws when administering an estate with international connections. Throughout this book the terms 'foreign resident' and 'non-resident' are used interchangeably and have the same definition. This anomaly in terminology occurs as Income Tax Assessment Act 1936 (Cth) ('ITAA 1936') uses the term 'non-resident' while Income Tax Assessment Act 1997 (Cth) ('ITAA 1997') primarily uses the term 'foreign resident'.